Corporate tax is based on a series of complex and ever-changing issues applicable to a wide and varied array of companies. Corporate tax often requires a specialist to best interpret its meaning and applicability.

German corporate tax is, simply put, the tax, payable on all income, which is levied on corporations including public and private limited companies, as well as cooperatives, associations and foundations. Partnerships and sole proprietorships are not subject to corporation tax, their liability rests in income tax.

In practice, however, corporate tax issues are far from simple. Their legal complexity will habitually require the application of specialist knowledge. For example, what is classed as income under tax law often runs contrary to the way earnings are determined under commercial law. An additional example of potential complexities within corporate tax is when, for tax purposes, separate companies may be treated as integrated fiscal units (Organschaft). An Organschaft is a similar concept to a consolidated group in the US.

Within an integrated fiscal unit one company, which is known as the controlled entity, agrees to be fully dependent on another, which then becomes known as the controlling company. Under such an arrangement, the controlled entity pays all its profits to the controlling company, which may also hold the majority of the voting rights in the controlled company. The effect of this deal for tax purposes is that the income of the controlled company is deemed to be that of the controlling company. Seen from the perspective of a client, this provides a method of balancing profits and losses across the fiscal unit. The intrinsic details surrounding structuring companies in order to benefit from the treatment as an integrated fiscal unit is where the requirement for specialists and consultants arises.

The corporate tax arena is a highly-intricate area of tax law and the need for specialist advice to help clients manage their tax exposure is of paramount importance if uncertainty is to be eliminated. Consultants and specialists have the ability to interpret tax laws and apply them directly to the clientele so as to tailor advice to each individual client, their company structure and their future business plans. WTS Group, one of the largest tax consultancies in Germany, which is represented internationally through alliances across various countries, is one such specialist firm advising on German corporate tax.

Unless you are one of the few corporations to be exempt from corporation tax, e.g. churches, sports clubs and charitable foundations, there is full liability to such a tax as a legal obligation. If this duty is not adhered to it can carry severe criminal fines for failure to pay the requisite tax sum. This obligation applies to all corporations domiciled or managed in Germany, and ensues that all their foreign and domestic earnings are all taxable within Germany.

Understanding one’s current tax liability and how this may change with planned company growth and development is imperative to managing exposure and will cut unnecessary extra costs. Specialist tax advisers can provide not only tailored advice to manage corporate taxation exposure, but can also offer counsel on how to format one’s legal entity structure to make it much more tax efficient. Good corporate tax consultants will have years of experience under their belt, which means they can put themselves into the position of their clients with more ease.

Taxation law is always a hot topic on the political constitutional agenda and is therefore constantly subject to change. One such example is the recent concern by the Supreme Tax Court surrounding the validity of the German minimum tax rule. The current minimum taxation rule prescribes that taxable income up to €1m can be completely offset by tax loss carried forwards and taxable income exceeding €1m can be offset up to 60 percent. This leaves only 40 percent of taxable income liable to tax. When this minimum rule is combined with rules on mergers, for example, this can result in an exclusion from a counterbalancing loss rather than merely deferring the actual loss, which is offset to the later period. It is for this reason that the minimum taxation rule has been seen as potentially unconstitutional. The Supreme Tax Court expressed in late 2010 that it had serious doubts regarding the constitutional validity of the minimum taxation rule.

Although that announcement does not constitute a binding decision, it does leave the door open for imminent change. This illustrates that the corporate tax landscape is constantly evolving. Therefore, businesses not working alongside corporate tax specialists can encounter considerable confusion on matters relating to such tax issues. Consequently, such experts should be consulted with regularity to help understand how to better manage taxation exposure.

A further example of the ever-changing landscape can be observed when trying to remain up-to-date on corporate tax issues surrounding withholding tax (WHT). Under current German corporation tax, when a German corporation pays dividends to corporate shareholders, it is subject to a 26.375 percent withholding tax. There is differential treatment between German corporations who can gain a full WHT refund and non-German corporations who may only reduce their liability to 15.825 percent.

Most recently, the ECJ ruled that such differential treatment violates the free movement of capital and called for refunds to be issued to companies under certain circumstances. Changes from the courts, coupled with the current political and economic European background within which Germany operates, make advice from specialists such as WTS Group imperative.

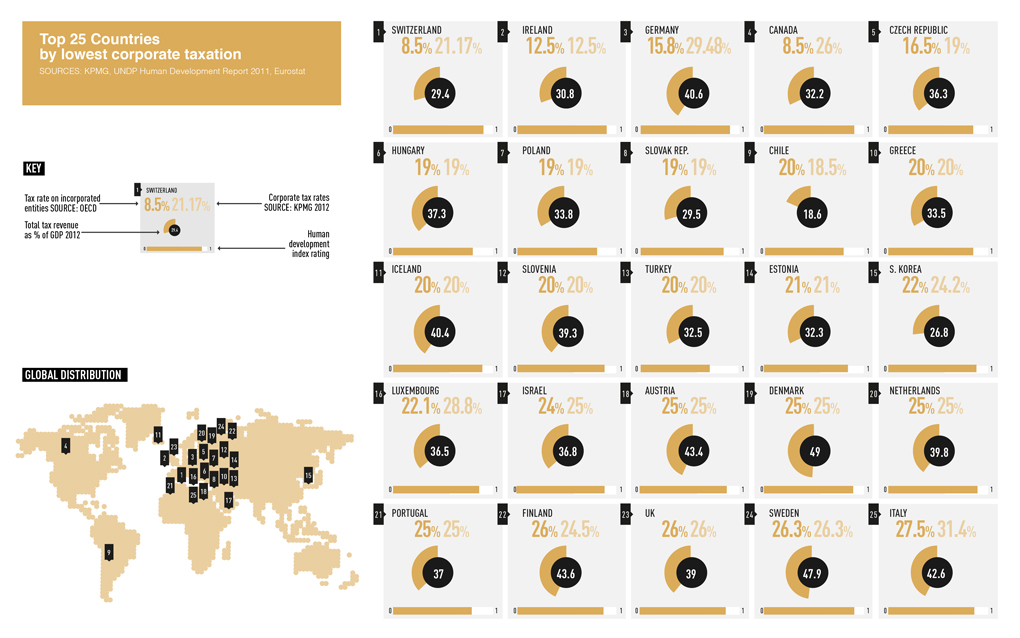

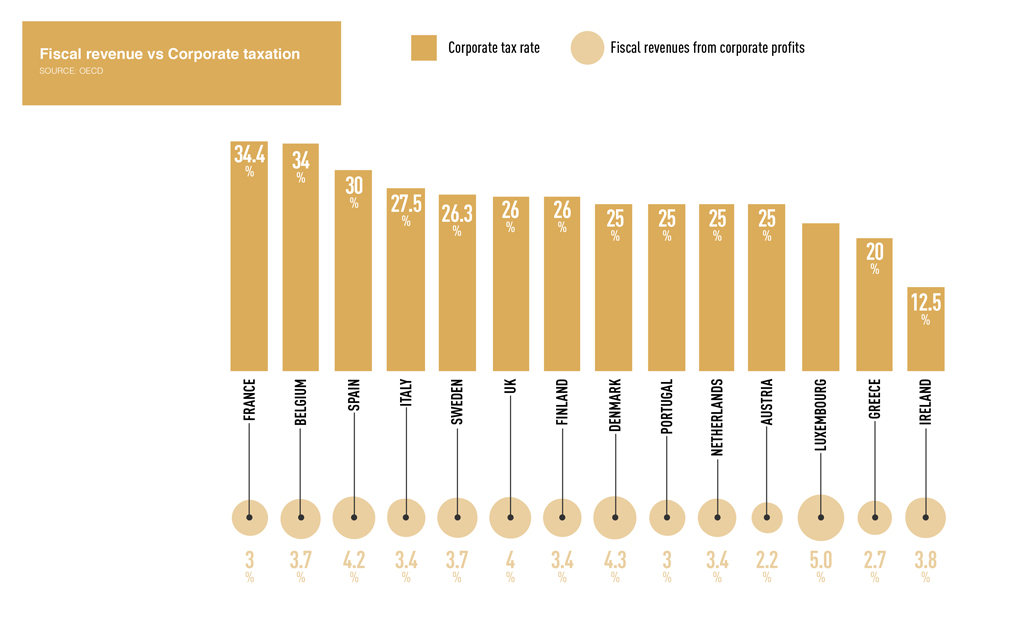

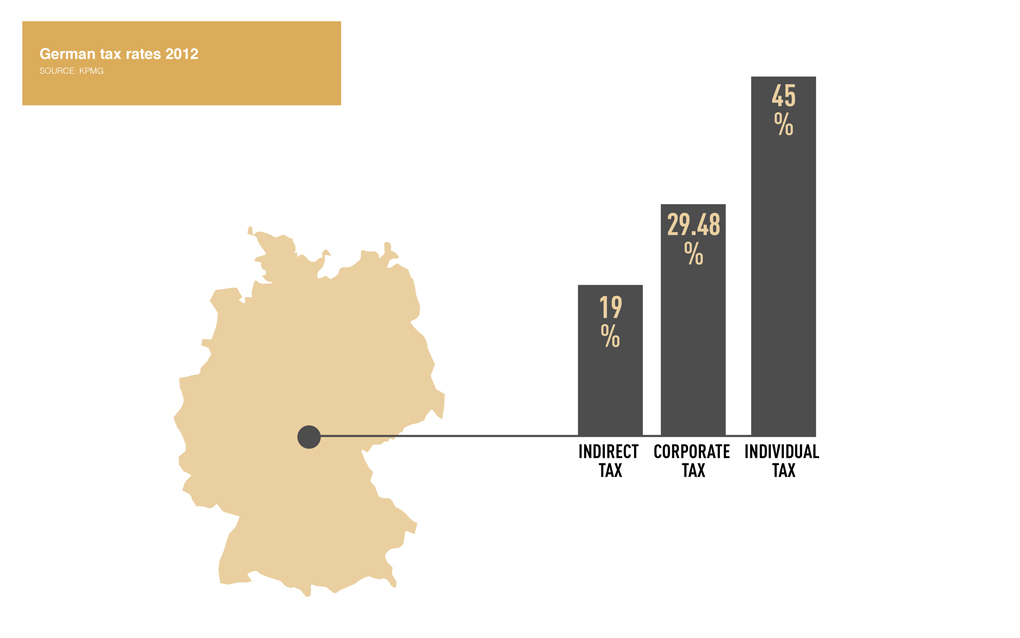

The federal taxation rate for corporations is a flat 15 percent calculated on an assessment year; that is, a calendar year ending on December 31. A further 14 percent to 17 percent, which is known as business tax, is payable to the municipality. The exact value of this business tax varies depending on the location of the corporate employees. Within this area there is a positive notion, in that business tax is deemed an allowable expense when calculating the income on which corporation tax is payable. In addition to the above taxes, a solidarity tax is also payable at 5.5 percent of the normal rate of corporation tax.

Therefore, all in all, the corporation tax rate, including the business tax and solidarity tax comes to around 30 percent to 35 percent.

In the case of dividends, where these are paid to a company with full corporation tax liability, the recipient is for the most part exempt from paying tax. During the tax assessment, five percent of dividends are added to profits as non-deductible operating expenses. Deducting tax from dividends which are paid by a fully tax-liable subsidiary parent domiciled in the EU can be waived under certain conditions. One such condition is that the parent company has to have a direct holding in the subsidiary of at least 15 percent.

Corporation tax is assessed based on the revenue which the corporate has earned during the calendar year. Thereafter, profits for taxable purposes are calculated using the outcomes from the annual accounts such as the balance sheets and the income statement, which are created under the Commercial Code.

The corporate tax payments are due in accordance with a notice for prepayments issued by the tax office. This obliges the taxpayer to pay quarterly payments on the outstanding tax on March 10th, June 10th, September 10th, and December 10th.

But the reduced rate for part of a corporation’s income, the waiver for deducting tax from dividends and the fact that solidarity tax is subject to special legal conditions, all renders these figures at best a mere hypothetical approximation. This demonstrates the importance of corporation tax advice from specialists such as WTS Group, which has vast experience in, and regularly deals with, German corporation tax legal provisions.

Most recently, tax experts have put forward reform proposals for the taxation of wealth in Germany. This quest for amendments is designed to produce additional annual tax revenues for the German state and to ensure that country’s wealthiest individuals contribute more in future to the financing of state budgets. Freshly published research by the Hans Böckler Foundation shows that although Germany’s private net wealth is four times public debt, the state nonetheless does not adequately tax large wealth, suggesting that German corporation tax is inadequate. The foundation’s study underlines that.

Thanks to low levels of wealth taxation, coupled with opportunities for corporations to legally evade tax, only 22 percent of income derived from entrepreneurial movement and investment pours directly to the tax authorities, compared to an estimated 45 percent from salary income. Further suggestions by the foundation asked for Germany to introduce a tax on financial transactions and to alter German corporate tax by reducing the tax breaks presently enjoyed by large companies with foreign subsidiaries.

Meanwhile, following a mediation committee meeting, the German Bundestag and Bundesrat have, at long last, approved the government’s amended 2011 tax simplification law. The bill was approved following a decision by the federal government to remove plans from the draft law to introduce a two-year abridged income tax declaration. The simplified law, das Steuervereinfachungsgesetz, came into force in Germany on January 1st, 2012, and includes measures which are intended to reduce the tax burden on both individuals and businesses as well as on the tax administration by an estimated €585m. The bill also provides for a €80 increase in the tax-deductible business expense allowance for employees, climbing from the previous €920 to €1,000.

In an attempt to further decrease the bureaucratic burden on both corporations and individuals the German government has now called for a second tax simplification package to be approved in 2012 to help simplify German tax law. A second series of measures was found to be needed when it was argued that the government’s first tax simplification law, the Steuervereinfachungsgesetz, was not adequate.

Schäuble has also pointed out that there are now pressing plans to amend the corporate tax law in order to make it simpler. A draft report is already being worked out which will outline a range of tangible suggestions. Although the finance ministry maintains that it is willing to consider any tax simplification initiatives, it has nevertheless stipulated that any proposals must be cost neutral and should not lead to a deficit in tax revenues to the German state.

Calls for tax harmonisation and convergence between Germany and France in the field of corporate tax, particularly regarding tax bases and rates, have been observed more frequently of late. The two nations have been debating on the establishment of a Common Consolidated Tax Base within the Union. The Green Paper on this business tax convergence has already been approved by Nicolas Sarkozy and Angela Merkel at the beginning of February. The key five priorities were the tax treatment of interest rates and dividends, partnership schemes, repayment rules, group schemes and the transfer of tax deficits. Legislative proposals on these areas are expected in both countries by 2013.

WTS Steuerberatungsgesellschaft mbH or WTS, is a globally renowned group of consulting companies which functions in the business arena within taxes and business consulting. The group centres its extensive tax expertise to offer council and represent multinational corporations, domestic as well as international SMEs, and high net worth individuals and expatriates. WTS’s array of products and services has in recent times been extended considerably, namely in the business areas of M&A, investment tax law, private clients and non-profit organisations. These areas of specialism are an added bonus to the already existing expertise offered by the highly client friendly team at WTS. German corporate law is, of course, among their specialties.

With well over 400 staff across seven German offices, the group of WTS professional companies is considered one of the biggest and most pre-eminent international tax consulting practices in the country. Thanks to its international associations, WTS can provide its client base with both regional and international expertise within an estimated 90 countries. Clients have the advantage that WTS focuses entirely on tax consultancy services, which helps to avoid any possible underlying conflicts with auditing activities.

What puts WTS ahead of the game within the area of corporate taxation is that, unlike its rivals, it wholly centres its practice on tax consultancy services. It has proven time and again that it can take the leading role within an international network of selected tax consulting firms. It also stands out for the standard of its consultants, who possess years of know-how within the corporate tax departments of companies operating on the international tax and consulting stage. This allows for a more perceptive understanding of client needs and creates a more proactive rather than reactive atmosphere.

The group’s unique and proactive approach to tax consulting makes for an inimitable contribution towards reducing tax-related perils on behalf of its highly-sophisticated clientele. The team of advisors at WTS is made up of highly practised generalists and dedicated authorities from major companies, consulting firms and the tax administration. Its expert consultants include tax advisers, tax representatives and solicitors. The clientele gains access to an extremely resourceful global network, while continually being led by WTS.

In addition to outstanding corporate tax advice, proficiency is offered also in a vast array of other tax business areas and include second-to-none expertise in transactions, integrated tax services, real estate taxation, asset management and financial services, supply chain strategy, governance and compliance advisory, and private client and HR tax services. Meanwhile, consulting encompasses accounting services, process and risk management, financial advisory, and restructuring and turnaround management.

WTS values its workforce and knows that it is the guarantee for the success of its business. It is because of this that it places high emphasis on training and excellent qualifications for all its employees. They in turn work devotedly and efficiently at the highest professional level, trying to serve their clientele’s needs. Clients will value the professionalism within this team of experts and will perceive them as priceless business partners. Moreover, it will become clear that employees at WTS employ a solution-orientated approach, yet another aspect that sets the WTS team apart from its competitors. Meanwhile, the group maintains a high degree of personal thoroughness and transparency at all times.

Most specifically, the WTS team focuses on advising HR departments and private high net worth clients. All of the above necessitate reliable and knowledgeable tax and legal councillors. Among the group of wealthy clientele, the WTS team advises corporations, managers, CEOs and private individuals.

The representation among others focuses on tax optimisation or local and global investments, charitable activities and business succession. In addition to considerations about income tax statements support is also given in issues concerning cross border relocation, tax audits, fiscal change of status, double taxation and matters relating to residency. It moreover proffers council on deferred compensation, pension planning and share-based payment instruments, including stock awards, phantom stocks and various other stock options.

But the remit of WTS reaches beyond German corporate tax and the other areas mentioned above. WTS understands that companies and its management face continuous challenges relating to their cross border tax planning. Global tax planning is an essential step for expanding companies. WTS has the ability to recommend which corporate structure and which group structure the correct one would be for any given client. It can also guide clients as to the most effective tax rate and provide assistance on matters connected to intellectual property.

Ongoing advice on group and corporate taxation

WTS offers clients advice during the set-up of companies regarding the most tax efficient legal form. It moreover deals with the taxation of corporations, the development of national and cross-border tax strategies and gives advice on reorganisations and on tax efficient financing. To its multinational clientele it also offers advice on national and international tax consolidation and group taxation.

Advice is also provided by the team on holding locations and structures as well as tax audits and remuneration schemes.

An area of focus for the WTS team within corporate taxation is counsel on the cross-border arena of projects in the plant and machinery construction industry. The team undertakes the calculation of taxes upon submission of project offers and looks into the structuring of projects with regard to the establishment or avoidance of permanent establishments. It also has a thorough comprehension of the process of profit splitting between head office and permanent establishments for both foreign and domestic tax purposes. In addition, it provides tax advice on project deployments with respect to both corporate taxation and the individual taxation of the expatriates.

International tax advice

Other tax counsel includes international tax advice, which focuses on advice regarding the selection of the most tax efficient form of foreign investments and on tax efficient foreign investment locations with respect to local regimes of tax relief. WTS will also offer unmatched advice on how to best prevent the application of Controlled Foreign Corporation (CFC) taxation pursuant to the German Foreign Tax Relations Act (Das Außensteuergesetz). Additional areas include the optimisation of group structures with regard to tax exemption of dividends and capital gains, tax deductibility of expenses and loss utilisation, and representation on the acquisition of foreign participations, cross-border distribution structures, transfer pricing, and expertise on the tax laws of foreign jurisdictions.

Additionally, the WTS team has widened its understanding in areas regarding suitable company and wealth succession, customising prenuptial agreements, contractual agreements relating to inheritance tax law, wills and articles of association. Within inheritance law, the group is skilled at providing thorough, up-to-date representation on gift tax law and related issues.

Key expertise

A standout individual within the WTS tax consulting group of companies is tax law expert Dr Alexander Hemmelrath. Renowned for carrying a wise head on his shoulders, Hemmelrath leads an experienced team of well-versed mentors and specialists. The head of tax consulting focuses within the field of private clients and HR tax services. This entails a wide spectrum of services which incorporate payroll tax advice, succession topics, tax-optimised wealth and executive private tax advisory. Individuals within his team proffer comprehensive consulting services in a broad array of tax and legal matters, including corporate taxation, to entrepreneurial families, private clientele and owner-managed businesses. Dr Hemmelrath was honoured in 2010 with the award for “Best Accountancy and Tax Advisor in Germany” from the prestigious business magazine European CEO. He was moreover awarded the World Finance Legal Award “Best Lawyer in Germany” in 2011 for the second time.